If You Read One Article About The Economic Crisis....

Make it this one.

Increasingly over the past several weeks, my favorite blog has become Baseline Scenario, written by Simon Johnson and James Kwak. Johnson was the chief economist at the IMF and now teaches at MIT, while Kwak is a student at the Yale Law School. And throughout this crisis, the two have consistently offered the best explanation of the financial crisis, how we got here and what we must do to get out. Many writers of this stripe argue on the basis of policy and which resolution is most likely to be the most cost-effective and successful. What sets Johnson and Kwak apart has been their ability to properly contextualize the crisis as a failure of elites, who grew too rich and too powerful and must be made to take losses, as a necessary component, indeed the only component, to revitalizing the American economy. Johnson has now put those thoughts into The Atlantic, in something of a long summary of the work of Baseline Scenario over the past few months, a description of how the financial industry took over the government, much like in most banana republics, and how the only way to properly wind this down is to shrink the power and influence of the industry, as would be done in any other emerging country when the bankers grow too big and the elites start stealing everything. This is must reading.

Kwak sets it up on his site.

From 1945 until around 1980, the financial sector was one industry among many in the United States. Then something happened.

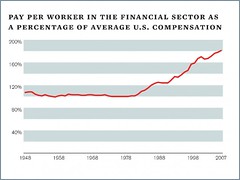

People in finance started making more money, jobs in finance became more desirable, financial institutions became more influential, and the linkages between the financial sector and the political establishment became stronger. At the same time that our financial sector became more leveraged and more risky, it also became more powerful. The result was a confluence of interests between Wall Street and Washington - one more normally found behind the scenes of emerging market crises, the kind the IMF is called on to resolve.

The chart shows that pay in the financial sector has risen to 181% of the average for all domestic private industries. They didn't just get too big to fail, they got way too big.

This is a familiar story to those who have been paying attention, but I've never seen it captured better. As the elite financiers grew richer and concentrated their wealth, they became more embedded with the government, not just with campaign contributions but through a shared belief system which made an unlimited virtue out of the unfettered free market. Certainly there has been a revolving door between Washington and Wall Street (and also at the top levels of academia, with econ professors shuttling in and out of financial institutions), but concurrent with that has been this image of Wall Street as a bunch of virtuous benefactors of their will, of the Masters of the Universe who can do no wrong.

Once, perhaps, what was good for General Motors was good for the country. Over the past decade, the attitude took hold that what was good for Wall Street was good for the country. The banking-and-securities industry has become one of the top contributors to political campaigns, but at the peak of its influence, it did not have to buy favors the way, for example, the tobacco companies or military contractors might have to. Instead, it benefited from the fact that Washington insiders already believed that large financial institutions and free-flowing capital markets were crucial to America’s position in the world [...]

Wall Street is a very seductive place, imbued with an air of power. Its executives truly believe that they control the levers that make the world go round. A civil servant from Washington invited into their conference rooms, even if just for a meeting, could be forgiven for falling under their sway. Throughout my time at the IMF, I was struck by the easy access of leading financiers to the highest U.S. government officials, and the interweaving of the two career tracks. I vividly remember a meeting in early 2008—attended by top policy makers from a handful of rich countries—at which the chair casually proclaimed, to the room’s general approval, that the best preparation for becoming a central-bank governor was to work first as an investment banker.

A whole generation of policy makers has been mesmerized by Wall Street, always and utterly convinced that whatever the banks said was true. Alan Greenspan’s pronouncements in favor of unregulated financial markets are well known. Yet Greenspan was hardly alone. This is what Ben Bernanke, the man who succeeded him, said in 2006: “The management of market risk and credit risk has become increasingly sophisticated. … Banking organizations of all sizes have made substantial strides over the past two decades in their ability to measure and manage risks.”

Over the past several decades and thanks to this shared ideology, finance has been massively deregulated, what regulations remained in place were never followed, institutions were allowed to grow in an almost unlimited fashion, leverage themselves tremendously, and "innovate" with exotic instruments that nobody truly understood. Every policy, seemingly, benefited the financial sector to an outsized degree. And every policy that would have limited the sector was quietly set aside.

Of course, what's best for the financial titans has never been what's best for the country, and this is true for any nation on Earth, many with which Johnson has real-world experience. The key to every financial crisis lies in that moment when the need for solutions runs up against a politics that practically exists to protect and defend elites.

Typically, these countries are in a desperate economic situation for one simple reason—the powerful elites within them overreached in good times and took too many risks. Emerging-market governments and their private-sector allies commonly form a tight-knit—and, most of the time, genteel—oligarchy, running the country rather like a profit-seeking company in which they are the controlling shareholders. When a country like Indonesia or South Korea or Russia grows, so do the ambitions of its captains of industry. As masters of their mini-universe, these people make some investments that clearly benefit the broader economy, but they also start making bigger and riskier bets. They reckon—correctly, in most cases—that their political connections will allow them to push onto the government any substantial problems that arise [....]

Squeezing the oligarchs, though, is seldom the strategy of choice among emerging-market governments. Quite the contrary: at the outset of the crisis, the oligarchs are usually among the first to get extra help from the government, such as preferential access to foreign currency, or maybe a nice tax break, or—here’s a classic Kremlin bailout technique—the assumption of private debt obligations by the government. Under duress, generosity toward old friends takes many innovative forms. Meanwhile, needing to squeeze someone, most emerging-market governments look first to ordinary working folk—at least until the riots grow too large [...]

From long years of experience, the IMF staff knows its program will succeed—stabilizing the economy and enabling growth—only if at least some of the powerful oligarchs who did so much to create the underlying problems take a hit. This is the problem of all emerging markets.

We have a far more developed country than those the IMF typically counsels, in some respects. Yet with the rise of an unaccountable and impenetrable oligarchy of elites, with a political class unwilling to do anything that would upset them, America resembles very closely the developing nations in banana republics. This continued fealty to the banks represent the leading threat to economic recovery. Whether through stoking fear of their failure or outright intimidation of the policymakers or something in between, the banksters own the country.

Johnson has his own prescriptions for the way forward: nationalizing the insolvent banks (which won't be cheap, but neither will any alternative), resolving the assets and returning them to private hands, increased regulation, etc. But none of that will work without the total and utter breakup of the oligarchy at the heart of the crisis.

Oversize institutions disproportionately influence public policy; the major banks we have today draw much of their power from being too big to fail. Nationalization and re-privatization would not change that; while the replacement of the bank executives who got us into this crisis would be just and sensible, ultimately, the swapping-out of one set of powerful managers for another would change only the names of the oligarchs.

Ideally, big banks should be sold in medium-size pieces, divided regionally or by type of business. Where this proves impractical—since we’ll want to sell the banks quickly—they could be sold whole, but with the requirement of being broken up within a short time. Banks that remain in private hands should also be subject to size limitations.

This may seem like a crude and arbitrary step, but it is the best way to limit the power of individual institutions in a sector that is essential to the economy as a whole. Of course, some people will complain about the “efficiency costs” of a more fragmented banking system, and these costs are real. But so are the costs when a bank that is too big to fail—a financial weapon of mass self-destruction—explodes. Anything that is too big to fail is too big to exist.

Johnson argues, compellingly, that President Obama is taking after the wrong Roosevelt, and what we need right now are the trust-busting policies of Teddy in addition to the New Deal policies of Franklin. But he ends on a downbeat note, mindful that the American oligarchy is much stronger, and the nation much less desperate, to expect the breaking of their money train to happen quickly or easily. It may take the threat of a real global collapse to shake us into action and away from this continued death-dance with the elites.

Anyway, read this and commit it to memory. To the extent that our political leaders listen at all anymore, they must understand how essentially untenable this economic power structure has become. I leave you with this quote from Mr. Johnson:

To paraphrase Joseph Schumpeter, the early-20th-century economist, everyone has elites; the important thing is to change them from time to time.

Labels: antitrust law, banking industry, DC establishment, financial industry, nationalization, Simon Johnson

dashed off by dday at 9:32 PM

![]()

![]() View blog reactions

View blog reactions

<< Home